Benefits of a CCP

The global financial crisis in 2008 unveiled three root causes of systemic risk: insufficient collateralisation, excessive risk-taking and a cumbersome web of interconnectedness among market participants. Since then, regulators, policymakers and market participants have joined together to address systemic risk and to prevent future crises with their associated costs. The primary tool to that end was the obligation of central clearing for OTC derivatives via CCPs.

Reduced Interconnectedness

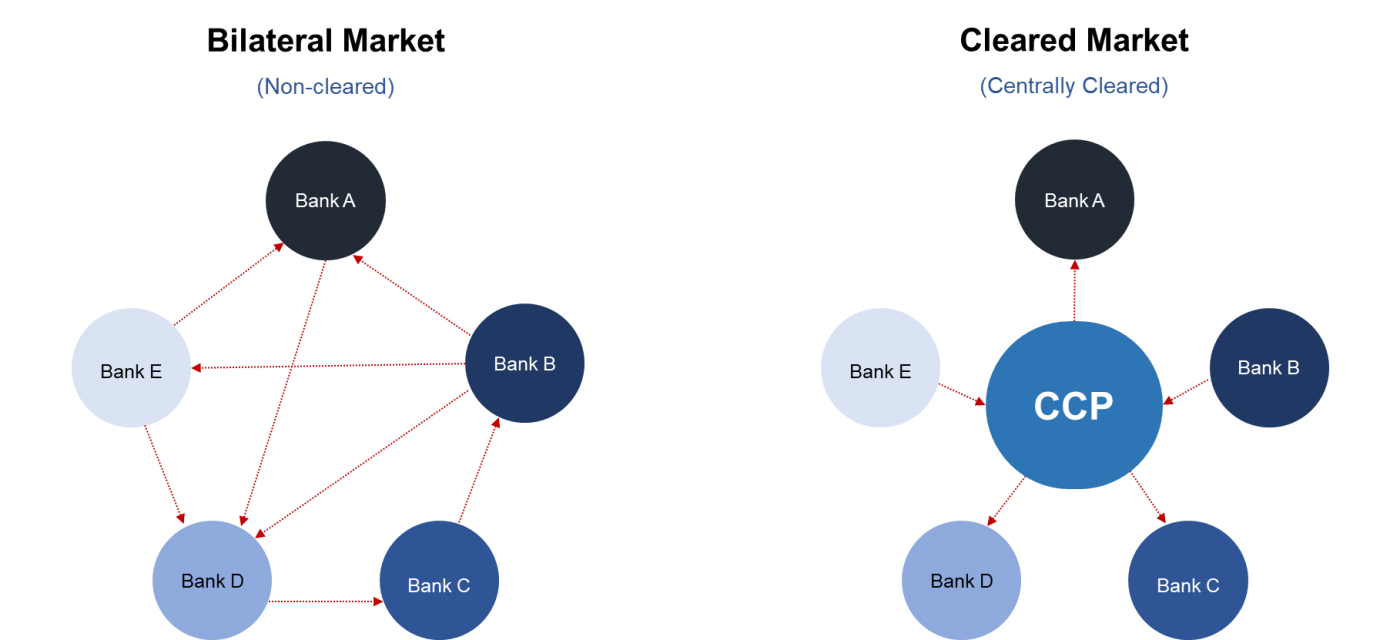

Financial interconnectedness is defined as the relationships among economic agents that are created through financial transactions and supporting arrangements. The impact of the failure of a large interconnected entity can serve as a conduit for contagion, spreading rapidly across the financial system and eventually leading to worldwide financial instability.

Central clearing directly reduces interconnectedness, thus protecting market participants in the event of default. CCPs act as risk managers, transparently keeping collateral from the original trading counterparties to secure the trades, and reduce risk exposure via multilateral netting.

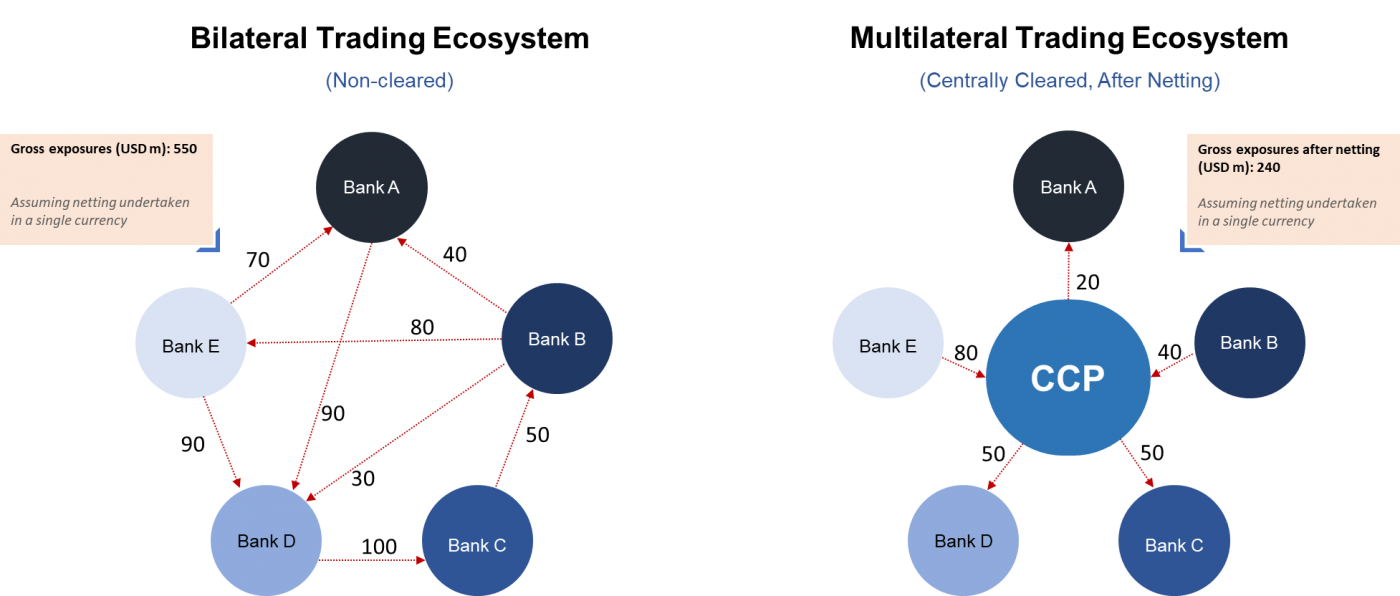

When trades are novated at a CCP, the resulting multilateral netting benefits can increase the operational efficiency and reduce counterparty credit risk, collateral requirements and liquidity needs of members. By removing the complex web of bilateral exposures into a single net exposure with the CCP, this creates an efficient ecosystem to manage trades. This offsetting of trades reduces the gross exposures significantly, resulting in a more streamlined and manageable trade infrastructure. This netting effect is commonly known as portfolio compression. Key benefits of multilateral netting include:

- Exposures: Exposures are based on net positions as opposed to the gross positions;

- Counterparty credit risk: Since the sum of the outstanding trades are significantly reduced, the counterparty credit risk is subsequently reduced;

- Administration costs: Since the costs associated with taking on new positions is on a per-trade basis, netted positions can reduce the overall administration costs for the counterparty, resulting in a more economical trade.

For further information on CCP interconnectedness, please read: Analysis of Central Clearing Interdependencies

Reduced Trade Processing

- Netting significantly reduces costs for trade processing and the collateral processing sides of the trade;

- Central clearing smooths operations while reducing the value of the obligations, which helps money move more efficiently among traders.

Improved Stability of Financial Markets

- Collection of margin collateral reduces systemic risk and prevents excessive risk taking;

- CCPs reduce contagion risk;

- Centralised default management tools limit uncertainty and foster confidence among members.

Transparency

- CCPs provide a holistic overview of the cleared markets (beneficial for regulators);

- CCPs have unique rulebooks instead of individual agreements with each counterparty;

- CCPs release Public Quantitative Disclosures (PQDs), in accordance with CPMI-IOSCO.

For more information on PQDs please see our CCP Global PQD page: here

Counterparty Access

- CCP clearing members do not need to rely on their own Know-Your-Client (KYC) checks for each new counterparty they trade with, since the CCP itself is the only legal counterparty.

Comprehensive Risk-Management

- CCPs manage counterparty risk through high levels of risk modelling and by ensuring resources are sufficient to withstand the loss of the two largest clearing members (Cover-2)

Trade Anonymity

- The counterparty to any end-buyer or end-seller is always the same – the CCP itself. This effectively provides trade anonymity for any clearing members.

For more information please see the CCP Global report: Incentives for Central Clearing at the Evolution of OTC Derivatives