Central Counterparties

Financial Market Infrastructures

Financial Market Infrastructures (FMIs) are critical to the security and stability of the financial markets they serve.[1] They underpin the economy and have a significant role to promote safe and efficient markets in addition to reducing contagion. FMIs consist of a range of financial entities, of varying systemic importance, these include: Payment Systems, Central Securities Depositories (CSDs), Securities Settlement Systems (SSSs), Trade Repositories (TRs) and Central Counterparties (CCPs).

What is a CCP?

A CCP is an FMI which interposes itself between the buyer and the seller of a trade. This process, known as novation, represents the major distinction between CCPs and Clearing Houses, the latter being financial institutions that guarantee trade settlement without becoming part of the trade. The CCP functions very closely with the exchange and trading system in order to novate the trades from the buyers and the sellers. A subsequent multilateral netting benefit is applied by the CCP which subsequently reduces the complexity of offsetting positions into one overall position.

Bilateral trading can be extremely complex with a web of trades occurring in a variety of currencies with complicated collateral being posted or received. If a counterparty were to fail in a bilateral trade, there would be no default management procedure. Therefore, CCPs offer a security net to act as the buyer to every seller and the seller to every buyer for every exposure.

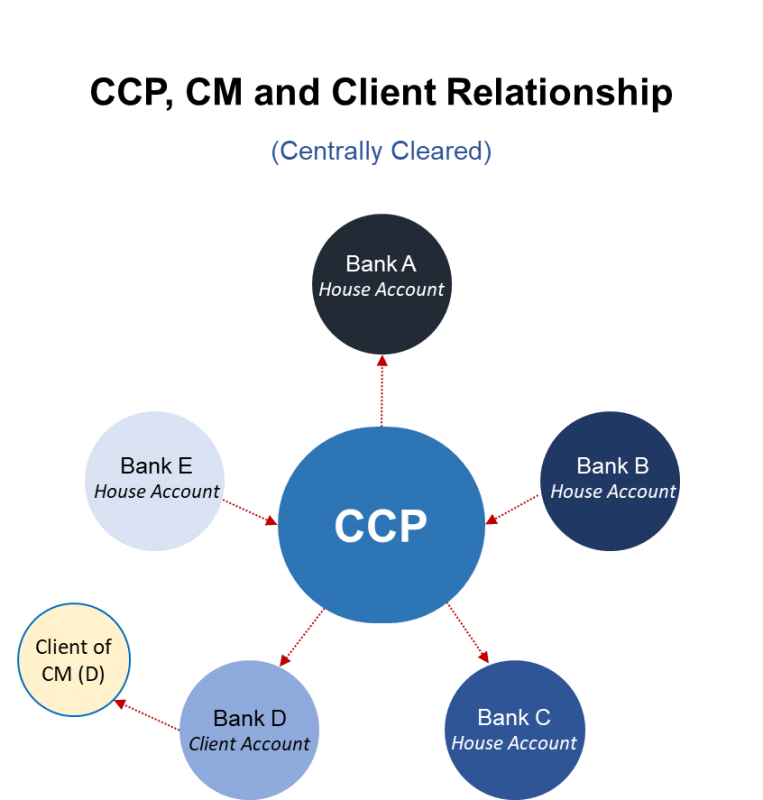

CCPs have relationships with a relatively small number of clearing members (CMs) (primarily investment banks and/or commercial banks). These members are approved by the CCP and are able to clear the trades from their own books, their client’s trades and the trades of non-clearing members (NCMs).

Non-clearing members (NCMs) are not affiliated with the CCP directly and are not permitted to clear their trades directly at the CCP. NCMs require a clearing account so that they can clear their trades through an appointed CM, if the CM chooses to offer client clearing. Subsequently, a house account is defined as the trades the CM clears for itself. The client account(s) are the trades the CM clears on behalf of their clients.

Please see Figure 2, where the trades have been novated.

The CCP acts as the guarantor to every trade with each respective member or counterparty (the buyers and sellers). If any of the clearing members were to fail to meet their trade obligations to the CCP, then the default management process (DMP) would be triggered which includes the process by which financial resources are utilised from the defaulted member, the CCP and non-defaulting clearing members’ resources where applicable; until the CCP can reach a ‘matched-book’. It is important to note that the DMP implementation phases differ from market-to-market and depends on a number of factors including, but not limited to: the number of clearing members pertaining to the CCP, the cleared product types on offer and the different regulatory and/or legal landscape.

For further information on the DMP, please view our section on: CCP Lines of Defence

[1] CPMI-IOSCO – Principles for financial market infrastructures; Rehlon, A., & Nixon, D. (2013). CCPs: what are they, why do they matter and how does the Bank supervise them?